Future Taxes Are a Huge Unknown - Especially in our Present economic Climate

Let’s drive to find out how they work...

We all know:

- Are IULs a SCAM? Here’s What People Get Wrong

- The 7 Big Myths About IULs — Debunked by a Licensed Insurance Strategist

- 4 Financial Problems an IUL Solves That 401(k)s and IRAs Can’t

- IUL vs. 401(k): Which Helps You Keep More of Your Money Long-Term?

1. How They Work (Simple Breakdown)

🟧 How a 401(k) Works

A 401(k):

- is tied directly to the stock market

- grows tax-deferred

- is funded with pre-tax dollars

- gets taxed when you withdraw

- penalizes you for touching it before 59½

In short, you get growth upfront and taxes later.

🟦 How an IUL Works

An IUL:

- earns interest based on an index

- gets market upside with a 0% downside floor

- grows tax-free

- provides tax-free access

- includes a guaranteed death benefit

- offers living benefits

Short version: it’s a tax-free growth + protection tool, not a tax-deferred gamble.

2. The Tax Question (The Biggest Difference of All)

🟥 401(k) Tax Reality

A 401(k) is basically a loan from the IRS.

They let you put money into a tax-free account now…

So they can tax you on a much larger amount later.

Think about that.

You’re deferring taxes on:

- your contributions

- Your employer match

- your growth

- possibly 30–40 years of compounding

People don’t retire in a lower tax bracket anymore.

And with national debt rising, tax rates are expected to increase significantly.

🟩 IUL Tax Advantage

An IUL, when properly designed, offers:

- tax-free growth

- tax-free access

- tax-free income

- tax-free death benefit

This is all thanks to IRS Section 7702.

Your retirement income could be 100% tax-free.

That alone makes IULs a powerful companion to traditional plans.

Indexed Universal Life▪️IUL = Downside Protection▪️IUL = Tax-free Growth ▪️IUL = Long-term Financial Flexibility

It’s not for everyone — but it’s absolutely not a scam.

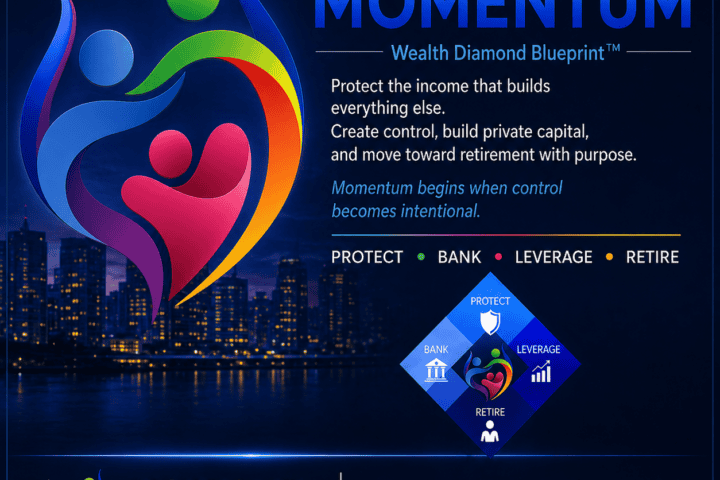

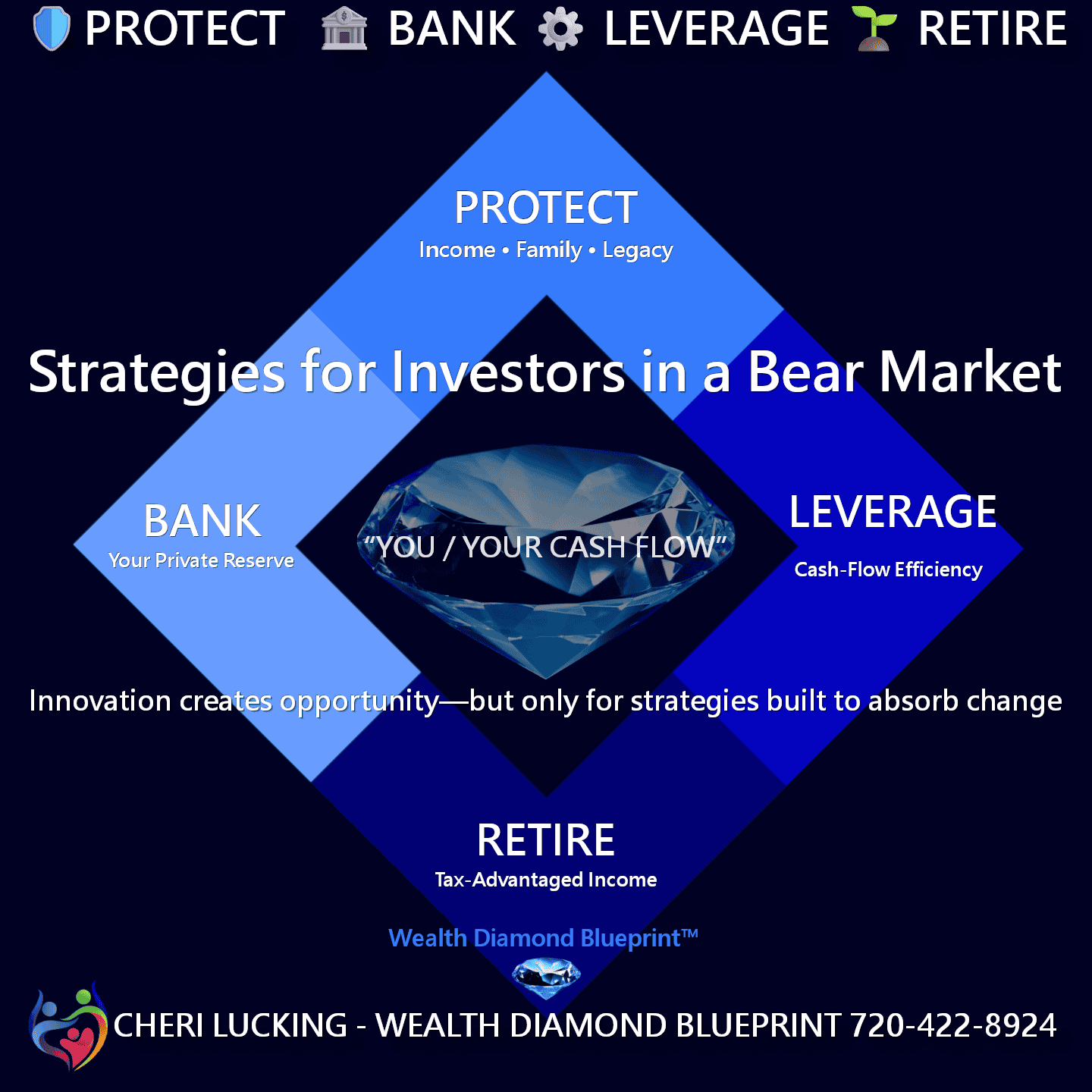

As part of the

Wealth Diamond Blueprint™ “cash-flow strategy”

It’s Probably Not for You!

CHERI LUCKING, CEO