Future Taxes Are a Huge Unknown - Especially in our Present economic Climate

Let’s bust the biggest misconceptions people repeat online.

🟥 The Problem With Traditional Retirement Accounts

Your 401(k) and IRA are tax-deferred—not tax-free.

This means:

- You postpone taxes until later

- But you don’t know what the tax rate will be

- And tax brackets are likely increasing (especially with TCJA expiring in 2026)

A 401(k) is essentially a joint account with the IRS.

Roth IRAs help, but:

- contributions are limited

- income restrictions apply

- high earners can’t shelter much

The government is in control—not you.

🟩 How an IUL Solves This Problem

IULs offer:

- tax-free growth

- tax-free access (via policy loans)

- tax-free retirement income

- tax-free death benefit

All under IRS Section 7702 rules.

No income limits.

No contribution restrictions.

No government penalties.

⭐ Why It Matters

When taxes rise, a tax-free income stream can be the difference between:

- retiring comfortably

- or having to reduce your lifestyle

An IUL puts you back in control.

Problem #3: Traditional Retirement Accounts Restrict Your Access to Your Own Money

🟥 Where 401(k)s and IRAs Fall Short

Try accessing your 401(k) before age 59½.

You’ll likely face:

- a 10% early withdrawal penalty

- income taxes

- reduced future compounding

- strict rules on how much and when

Even in retirement, Required Minimum Distributions (RMDs) force you to withdraw on the IRS’s schedule—not yours.

In short:

Traditional retirement tools lack liquidity and flexibility.

🟩 How an IUL Fixes This

With an IUL, you can access your cash value:

- at any age

- without penalties

- without government restrictions

- without disrupting policy growth

Through:

- withdrawals

- policy loans

- flexible repayment (or no repayment)

You can use your cash value to:

- fund a business

- buy real estate

- cover emergencies

- supplement income

- invest

- take advantage of opportunities

Your money is accessible when you need it—not when the IRS permits it.

⭐ Why It Matters

Life doesn’t wait until 59½.

Your retirement strategy shouldn’t either.

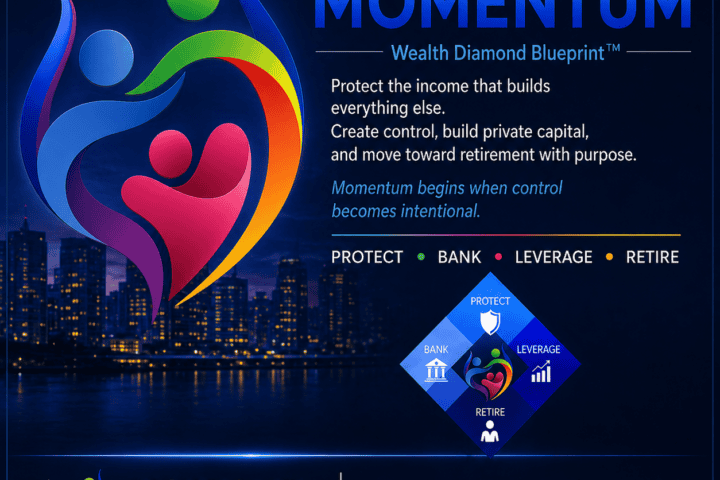

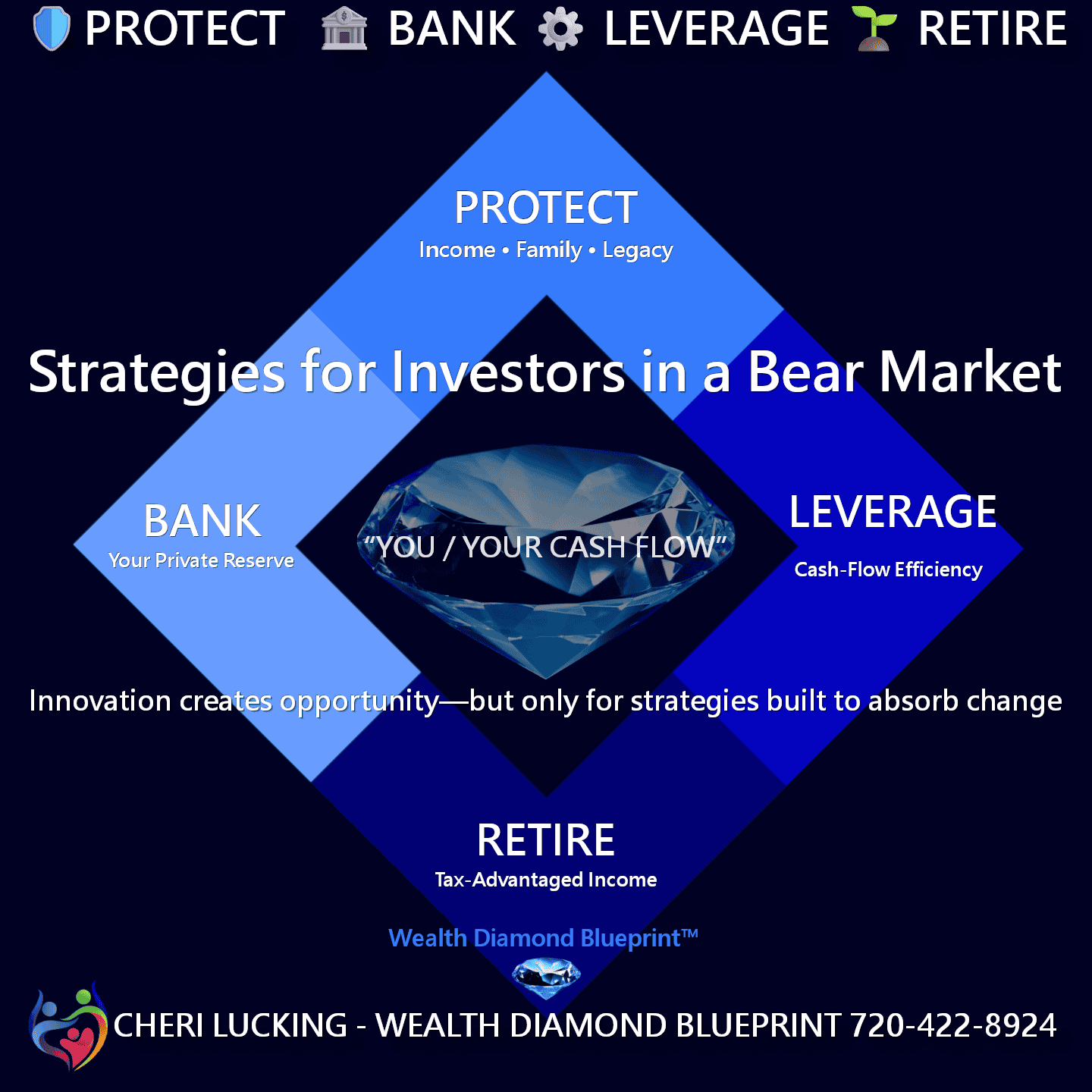

Indexed Universal Life▪️IUL = Downside Protection▪️IUL = Tax-free Growth ▪️IUL = Long-term Financial Flexibility

It’s not for everyone — but it’s absolutely not a scam.

As part of the

Wealth Diamond Blueprint™ “coordinated financial approach.”

It's Probably Not for You!

CHERI LUCKING, CEO