Benefit from Term Life, Whole Life or Indexed Universal Life IUL Insurance

Which is right for You? Term Life vs Whole Life vs Indexed Universal Life IUL

Understanding the differences between Term Life vs Whole Life vs Indexed Universal Life IUL Insurance can make or break your day. Unfortunately, you may realize your mistake 10 to 20 years later.

I’ve been there and made the mistake…

When my husband and I married, we chose a term life policy after consulting our insurance agent. Twenty years later, we realized that opting for whole life would have been better, as term life offered no cash value and cost us thousands.

As your insurance expert, I won't let this happen to you.

Quick Comparison: Term Life vs Whole Life vs Indexed Universal Life IUL

| Feature | Term Life | Whole Life | Indexed Universal Life (IUL) |

| Coverage Duration | Temporary (10, 20, or 30 years) | Permanent (for life) | Permanent (for life) |

| Premiums | Lowest cost initially | Fixed and higher than term | Flexible (can adjust over time) |

| Cash Value | ❌ None | ✅ Guaranteed cash value | ✅ Cash value grows based on the market index |

| Growth Potential | ❌ None | Moderate (fixed rate + dividends*) | Higher potential (based on index performance) |

| Investment Risk | ❌ None | ❌ None (guaranteed growth) | ❗ Market-linked, but with downside protection |

| Flexibility | ❌ Low | ❌ Low | ✅ High (adjust premiums and death benefit) |

| Loan Access | ❌ No | ✅ Yes (loan against cash value) | ✅ Yes (loan against cash value) |

| Expiration | Ends when the term ends | Never expires (as long as premiums are paid) | Never expires (as long as policy is funded) |

| Cost Over Time | Increases if you reapply when older | Fixed premiums | Can be structured for increasing or level cost |

* Dividends are not guaranteed; they only apply to participating in whole life policies.

Summary: Term Life vs Whole Life vs Indexed Universal Life IUL

Term Life Insurance - This Should Only be Temporary Fix

If you use Term Life Insurance long-term, you are wasting your money, as there are better solutions that may meet and even exceed your needs.

$$$ Term Life Insurance - The "Short-term fix" $$$

It generally has no "Cash Value"

"Term life insurance offers budget-friendly, short-term coverage that lasts for a set number of years. If the insured individual dies during this period, the policy pays a death benefit to their beneficiaries. - This should be treated as a short-term fix." – Cheri Lucking, Your Insurance Expert

- Great for: Temporary needs like covering a mortgage or young children.

- How it works: You pay a low monthly premium for a set time period (e.g., 10 years). If you pass away during that time, your beneficiary receives the death benefit.

- No cash value. When the term ends, your coverage also ends—unless you renew at a higher rate.

- If you decide to get term life insurance, ensure that it is convertible.

Whole Life Insurance

"Whole life insurance is a form of permanent coverage designed to last a lifetime. It offers both a death benefit for your beneficiaries and a cash value that accumulates over the years." - Cheri Lucking, Your Insurance Expert.

- Great for: Lifelong protection and building guaranteed savings.

- How it works: You pay the same premium for life. Part of that premium builds cash value, which grows tax-deferred and can be accessed via loans or withdrawals.

- Offers guaranteed death benefit, guaranteed cash value, and potential dividends (if from a mutual insurance company).

Indexed Universal Life (IUL)

"Indexed Universal Life (IUL) insurance is a type of permanent life insurance that provides ongoing death benefit protection alongside a cash value component. This cash value grows in relation to the performance of a selected stock market index, allowing for potential gains while also ensuring downside protection.

Additionally, IUL policies offer flexibility in premium payments to accommodate individual financial situations."

– Cheri Lucking, Your Insurance Expert.

- Great for: Lifelong protection and building guaranteed savings.

- How it works: You pay the same premium for Life. Part of that premium builds cash value, which grows tax-deferred and can be accessed via loans or withdrawals.

- Offers guaranteed death benefit, guaranteed cash value, and potential dividends (if from a mutual insurance company).

Summary: Which is best?

Without an insurance assessment, it's up to you to determine the benefit and cost. But if you would like an expert opinion, it's FREE, book a Call, one-on-one with me, Cheri, Your Insurance Expert

- Term Life → Budget-friendly for short-term needs

- Whole Life → Safe, guaranteed lifelong protection and savings

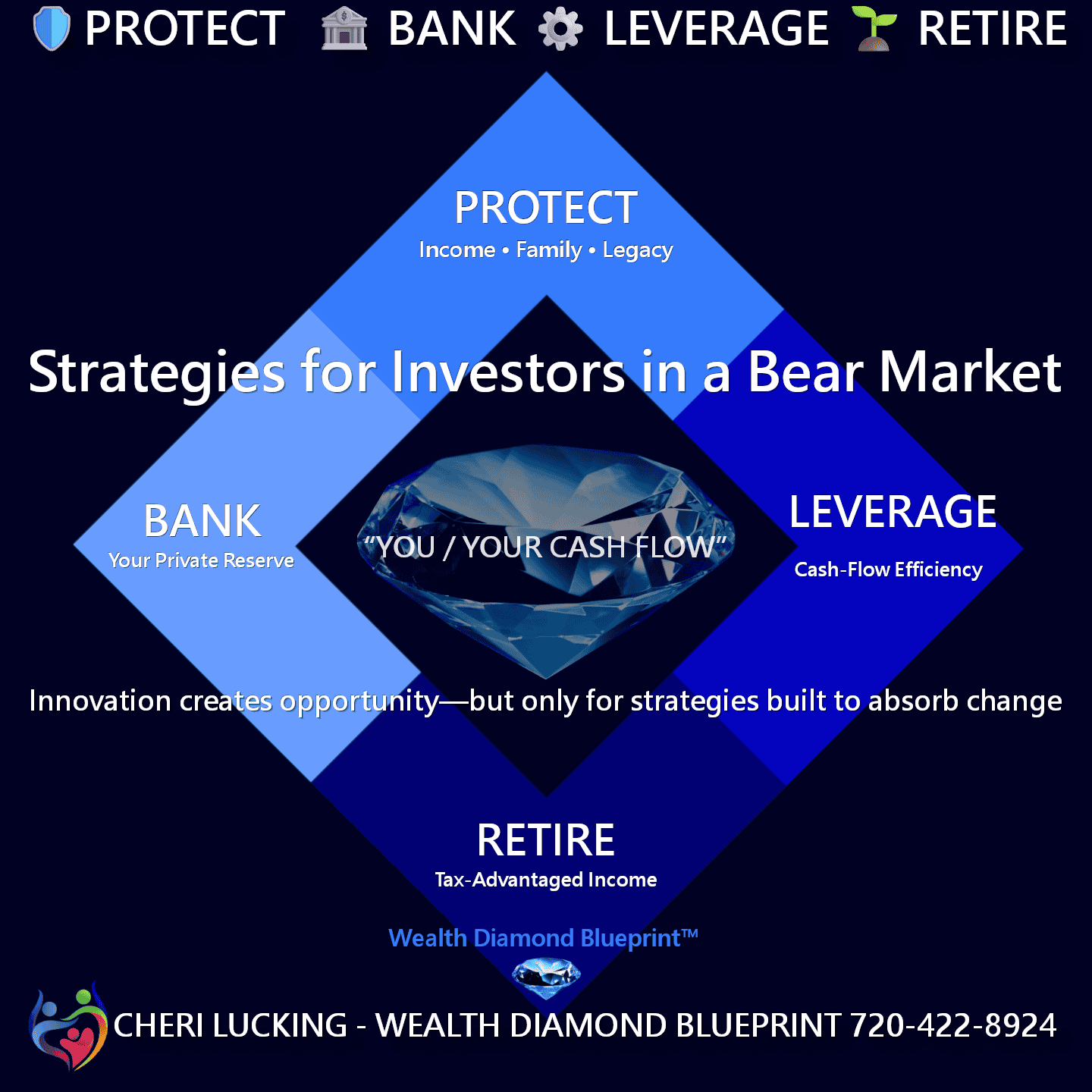

- Indexed Universal Life IUL → Long-term growth, flexibility, and a tax-advantaged retirement strategy, especially when combined with a Debt-Free Life Insurance Plan and Infinite Banking

I will always advise you based on your needs.

Ideally, I believe that you should finance your own lifestyle by using "cash value" life Insurance.

Let's Get Your Insurance Strategy Up To Date

Lucking Life Insurance - Protecting What Matters Most to You

Why You Might Want Both an Index Universal Life Insurance IUL and Infinite Banking Solutions?

ARE YOU READY TO PROTECT YOUR LIFE – YOUR GOALS – YOUR FUTURE

I help you take Control of Your Finances using Infinite Banking and Debt-Free Life solutions.

Especially

"When the Going Gets Tough"

Give Me a Call 720-422-8924

Let’s Chat – No Pressure, Just Peace of Mind

“Most families and businesses I speak with are surprised by The Game Changer, created by an Indexed Universal Life Plan (IUL) when combined with Infinite Banking or a Debt-Free Life Insurance Plan that contains an Indexed Linked Universal Life Policy with a Whole Life Insurance policy.

The extraordinary result is the Next Generation

of

Infinite Banking or Debt-Free Life Solutions

Let’s take 15 minutes to review your options—no obligations, just information that can help lower your debt, create and protect your legacy.

CHERI LUCKING, CEO

Related Services Links

- Your Life - Debt-FREE Life

- Your Life - Infinite Banking

- Your Life - A Plan for Business

- Your Goals - Enhance your wealth

- Your Goals - Protect Your Family ▪️ Mortgage Protection

- Your Goals - Financial Independence - Save Enough to Meet Your Needs

- Your Future - Ensuring Your Retirement Security

- Your Future - Ensure the Long-term Care We Need

- Your Future - Final Expense Life Insurance

Disclaimer: This content was generated using AI and Human Verification.

Article Author:

Cheri Lucking, CEO of Lucking Life Insurance, and Peter Lucking, Co-author/Web design, CEO, Content Branding Solutions

“Lucking Life Insurance is for Families looking for Mortgage Protection, Life Insurance, Retirement Income, Medical, Medicare Supplement policies, and Healthcare Plans to: Protect the ones you love – With Life Insurance Plans that are as unique as you.” – Cheri Lucking

Cheri Lucking Bio:

She is a published author and has held various roles in advertising, marketing, communications, sales, distribution, and product branding and development. Cheri lives with her husband, Peter, and their dog, Coco. Cheri enjoys cooking, gardening, hiking, and wine, although not always at the same time. She loves music and is an avid reader,

She would tell you, “I cannot live without eBooks.” Cheri agrees but would add cheese, the Food Channel, and nature to that list.

Cheri Lucking Insurance Weekly Newsweek

U.S. Insurance Industry News