Most homeowners don’t have a mortgage problem—they have a mortgage strategy problem.

What if this simple Strategy could help You

Discover a simple, client-friendly look at the strategy behind paying off your home faster—while protecting your family and building long-term wealth.

Most homeowners don’t have a mortgage problem—they have a mortgage strategy problem.

If you’re doing everything “right” (making the payment, staying consistent, trying to save when you can) but the payoff timeline still feels forever, you’re not alone. The traditional mortgage is designed so that a big portion of your early payments goes to interest, not ownership.

That’s why I like to teach a framework that’s easy to understand and personalized to your numbers: Protect Smarter → Pay Off Faster → Build Wealth. Here’s what that can look like in real life.

"Where should capital live so it can grow, stay accessible, and remain under my control?"

The Roadmap: Mortgage Protection → HELOC Strategy → Infinite Banking

- Mortgage protection: If your income stops, the plan shouldn’t fall apart.

- HELOC strategy (velocity-style cash-flow management): For the right homeowner, using cash flow intentionally may help reduce interest and shorten the payoff timeline—often by creating disciplined extra principal payments and (in some cases) small interest-efficiency gains through daily-balance interest calculations.

- Infinite Banking (long-term): A properly structured cash-value life insurance policy can create a personal pool of capital you can borrow against later, while keeping long-term growth and protection in place.

Quick note: This is educational, not financial or legal advice. Every mortgage, rate environment, and household cash flow is different—so the right approach is always the one that fits your situation.

3 steps to Paying off your Mortgage Faster

Step 1: Protect the Plan (Not Just the Payment)

When people get excited about paying off their home faster, they usually focus on one thing: the math. But there’s a second question that matters just as much: What happens if your income stops before the mortgage is paid off?

- If something happened to you tomorrow, would your family be able to keep the home?

- If you were out of work for 3–6 months, would the mortgage strategy still work?

- Are you protecting the entire plan—or just hoping nothing interrupts it?

Step 2: Pay Off Faster (A HELOC Strategy—When It Fits)

A common approach homeowners ask about is using a HELOC (Home Equity Line of Credit) as part of a “velocity-style” strategy: you use the line strategically, then route income through it to reduce the balance quickly, and repeat. Some versions use your HELOC almost like a primary checking account—income goes in, bills come out—so the average daily balance stays lower.

Why it can work (for the right person):

- Positive monthly cash flow (you consistently spend less than you earn).

- Strong discipline—because the system only works if you don’t treat the HELOC like extra spending money.

- A realistic rate/fee picture—HELOC rates are often variable, and fees/terms matter.

- Process clarity—many people see progress simply because they’re making consistent extra principal payments with better tracking and structure.

Important cautions: A HELOC is secured by your home. If cash flow gets tight, rates rise, or spending slips, it can create real risk. In today’s higher-rate environments, the “hack” may not outperform straightforward extra principal payments unless the numbers truly work after fees and rate changes.

Are You Ready?

Download your Check list Now!

Step 3: Build Wealth (Infinite Banking as the Long-Term Engine)

Infinite Banking is a strategy that uses a properly structured, cash-value life insurance policy (often a dividend-paying whole life policy) to create a personal pool of capital. Over time, the cash value can grow, and you may borrow against it for opportunities or expenses—while keeping protection in place.

Hi, I’m Cheri Lucking, I specialize in Advanced Insurance Strategies

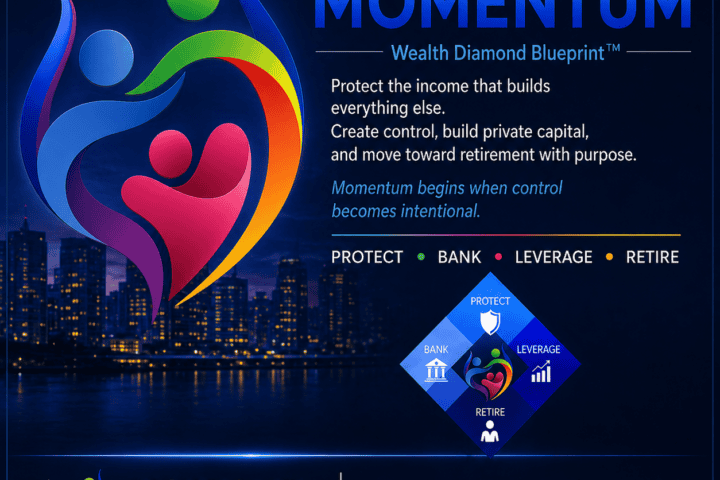

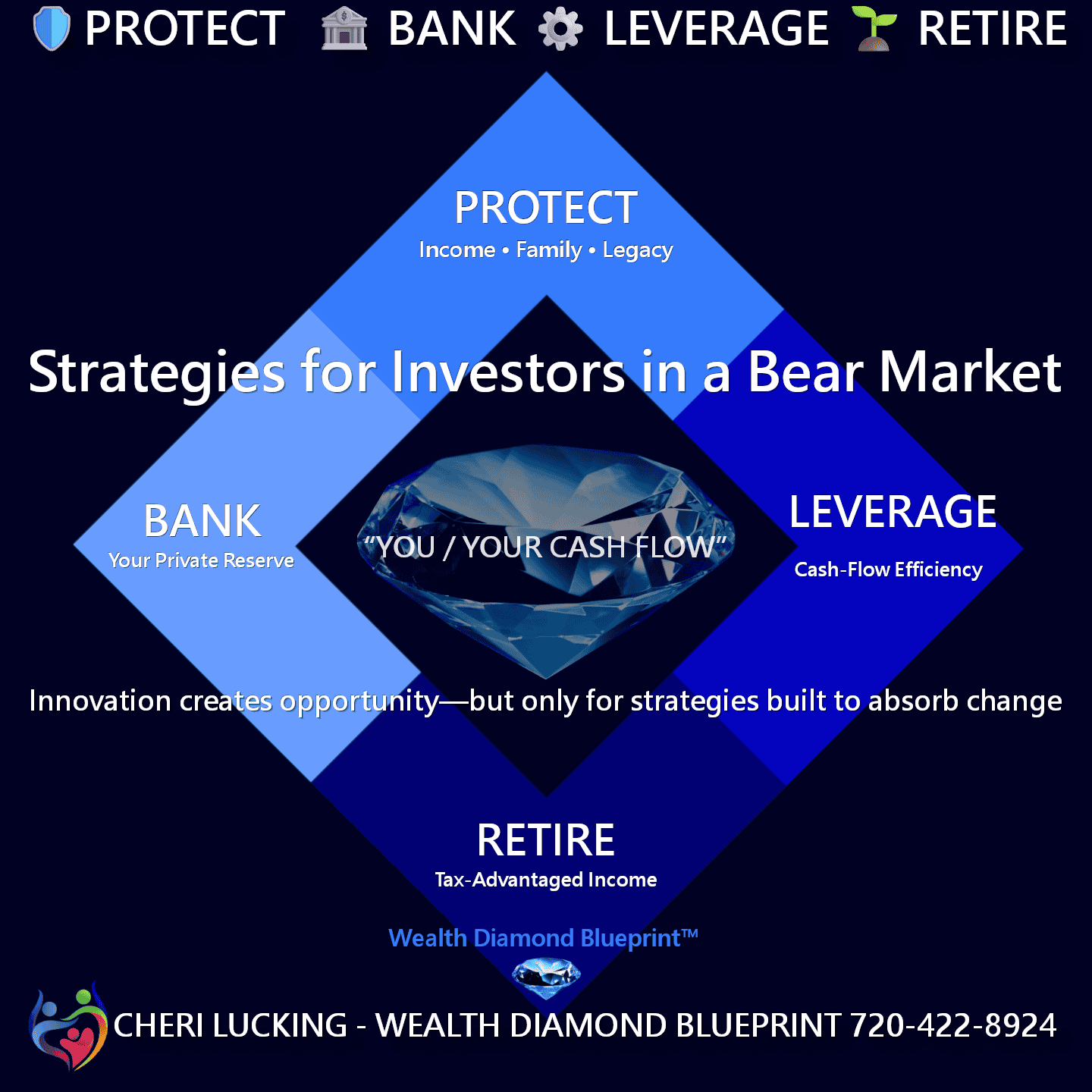

The Wealth Diamond Blueprint is one such strategy.

The Four Corners of the Diamond:

Protect - Safeguarding the Foundation of Your Financial Plan

Bank - Creating Control, Access, and Cash-Flow Efficiency

Leverage - Using Existing Assets More Intentionally

Retire - Building Reliable, Tax-Advantage Retirement Income

To Create Your

Wealth Diamond Blueprint™

A Cash-Flow Strategy for Financial Success,

and a Tax-Advantage Retirement

EXCELLENCE ▪ TRANSPARENCY ▪ HONESTY ▪ EXPERT ▪ INTEGRITY ▪ PERSONALIZATION ▪ PASSION

Discover the Benefits of Your Wealth Diamond Blueprint™

Create Your Living Blueprint to Success

Summary

Main idea: Most people aren’t stuck because of their mortgage—they’re stuck because they’re using the default strategy. Traditional mortgages are heavily interest-loaded in the early years, so progress can feel slow even when you’re doing everything right.

- Core framework: The approach is explained as a 3-part roadmap:

- Protect Smarter (Mortgage Protection)

- Pay Off Faster (HELOC / “velocity” cash-flow strategy, when appropriate)

- Build Wealth (Infinite Banking over the long term)

- Step 1: Protect the plan: Before focusing on payoff math, it asks: What happens if income stops? The point is to protect not just the monthly payment, but the entire payoff plan so the family can keep the home during disruption.

- Step 2: HELOC strategy (when it fits): A HELOC can be used to route income and expenses in a way that keeps the average daily balance lower and helps accelerate payoff—but only if the homeowner has consistent positive cash flow, strong discipline, and the numbers still work after variable rates and fees. It also highlights real risks since a HELOC is secured by the home.

- Step 3: Infinite Banking: Uses a properly structured cash-value life insurance policy to build a personal pool of capital over time. The cash value can grow and be borrowed against later while keeping protection in place.

- Disclaimer: It’s educational only; the “right” approach depends on the person’s mortgage, rates, fees, and cash flow.

If you’d like clarity on whether this approach makes sense for you, the next step is simply a conversation.

👉 Schedule a 30-Minute Cash Flow & Capital Strategy Call

(Education first. No pressure.)

📘 Explore the Private Reserve Banking Framework

Learn how Infinite Banking works alongside cash-flow strategies and long-term planning tools.

Once Debt Stops Dominating Cash Flow… You are ready for the Wealth Diamond Blueprint™

What if, this Strategy Makes Sense for You!

Schedule Your Diamond Blueprint to Success

The Secret the BANKS won't tell You!

The Secret Weapon: Tax-Free Retirement Through Life Insurance

Create Your Private Reserves and have a Tax-Free Retirement Through Life Insurance.

What if every dollar you ever "borrowed" for your business came from YOUR own private bank instead of theirs? And built Your TAX-FREE Retirement plan.

Lucking Life Insurance - Because Your Tomorrow Matters

Schedule your Wealth Diamond Blueprint Assessment today

Lucking Life Insurance - Protecting What Matters Most to You

Give Me a Call 720-422-8924

Let’s Chat – No Pressure, Just Peace of Mind

“Most families and businesses I speak with are surprised by The Game Changer, created by Private Reserves with Debt-Free Life Solutions, when combined with an Insurance Plan that contains an Indexed Linked Universal Life Policy with a Whole Life Insurance policy.

The extraordinary result is the Next Generation

of

Private Reserves with Debt-Free Life Solutions

Let’s take 15 minutes to review your options—no obligations, just information that can help lower your debt, create and protect your legacy.

CHERI LUCKING, CEO

Related Services Links

- Your Life - Debt-FREE Life

- Your Life - Private Reserves and Infinite Banking

- Your Life - A Plan for Business

- Your Goals - Enhance your wealth

- Your Goals - Protect Your Family ▪️ Mortgage Protection

- Your Goals - Financial Independence - Save Enough to Meet Your Needs

- Your Future - Ensuring Your Retirement Security

- Your Future - Ensure the Long-term Care We Need

- Your Future - Final Expense Life Insurance

Disclaimer: This content was generated using AI and Human Verification.

Article Author:

Cheri Lucking, CEO of Lucking Life Insurance, and Peter Lucking, Co-author/Web design, CEO, Content Branding Solutions

“Lucking Life Insurance is for Businesses, Entrepreneurs and Families looking to Protect the ones you love – With Life Insurance Plans that are as unique as you.” – Cheri Lucking

Cheri Lucking Bio:

She is a published author and has held various roles in advertising, marketing, communications, sales, distribution, and product branding and development. Cheri lives with her husband, Peter, and their dog, Coco. Cheri enjoys cooking, gardening, hiking, and wine, although not always at the same time. She loves music and is an avid reader,

She would tell you, “I cannot live without eBooks.” Cheri agrees but would add cheese, the Food Channel, and nature to that list.

Cheri Lucking Insurance Weekly Newsweek

U.S. Insurance Industry News